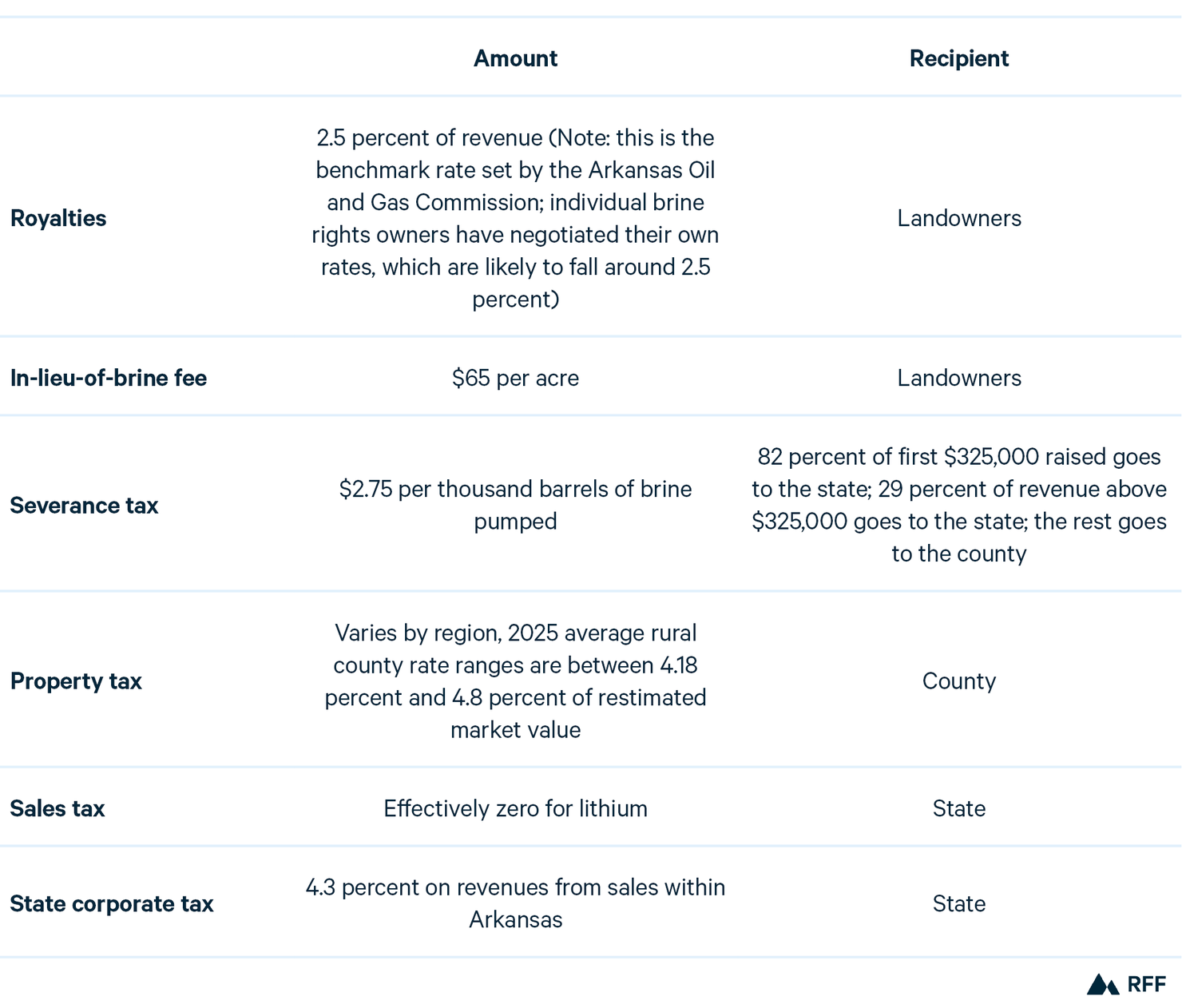

Table 1. Taxes and Royalties Collected

Table 2. Average Yearly Collected Revenues (Base Case for Southwest Arkansas)

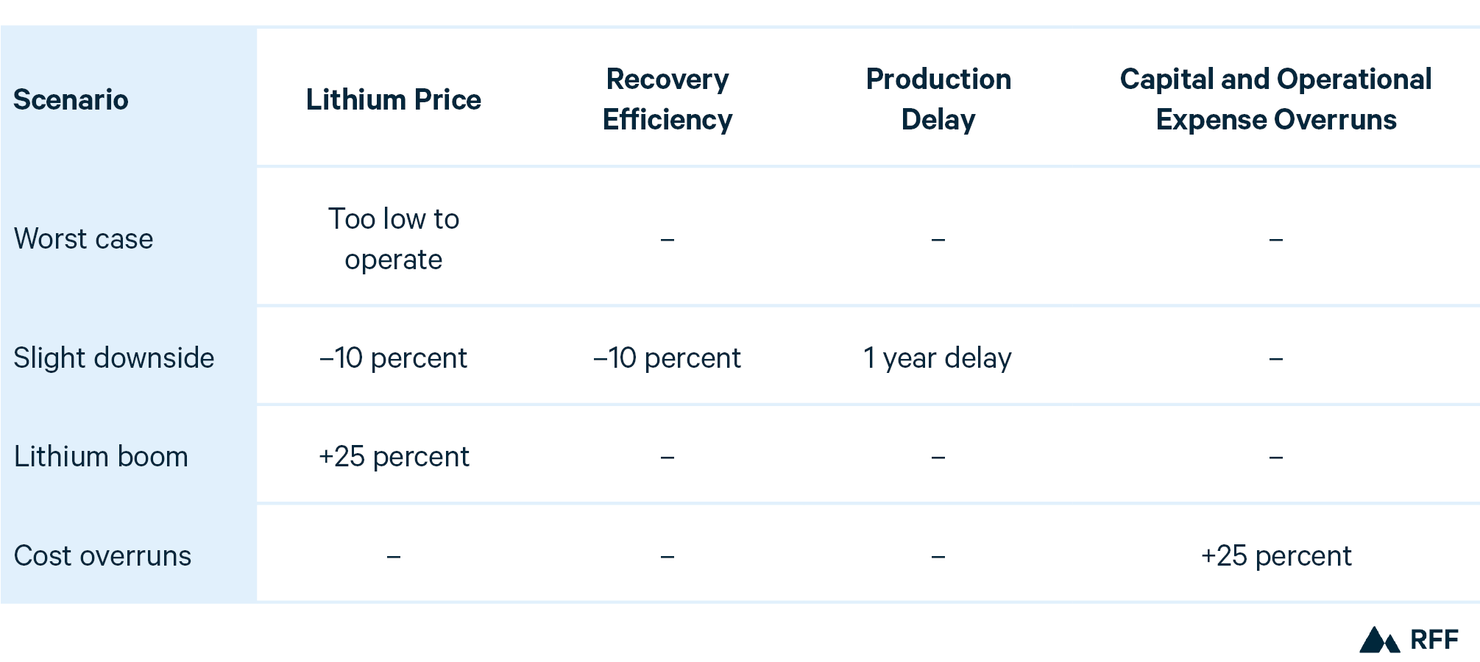

Table 3. Four Lithium Revenue Scenarios

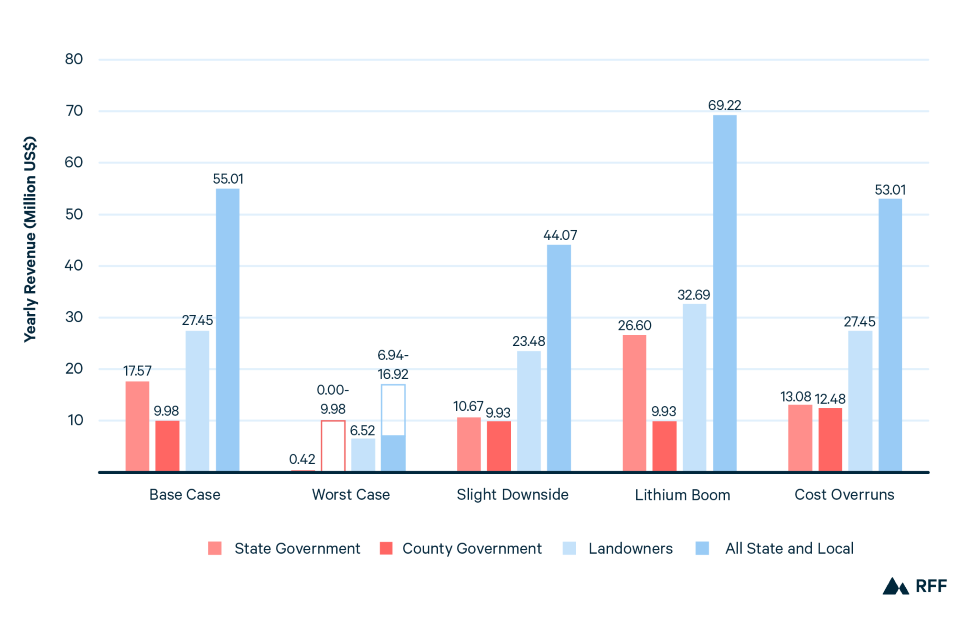

Figure 1. Yearly Revenues Collected by Landowners and Government from Lithium Extraction Under Different Scenarios for Southwest Arkansas

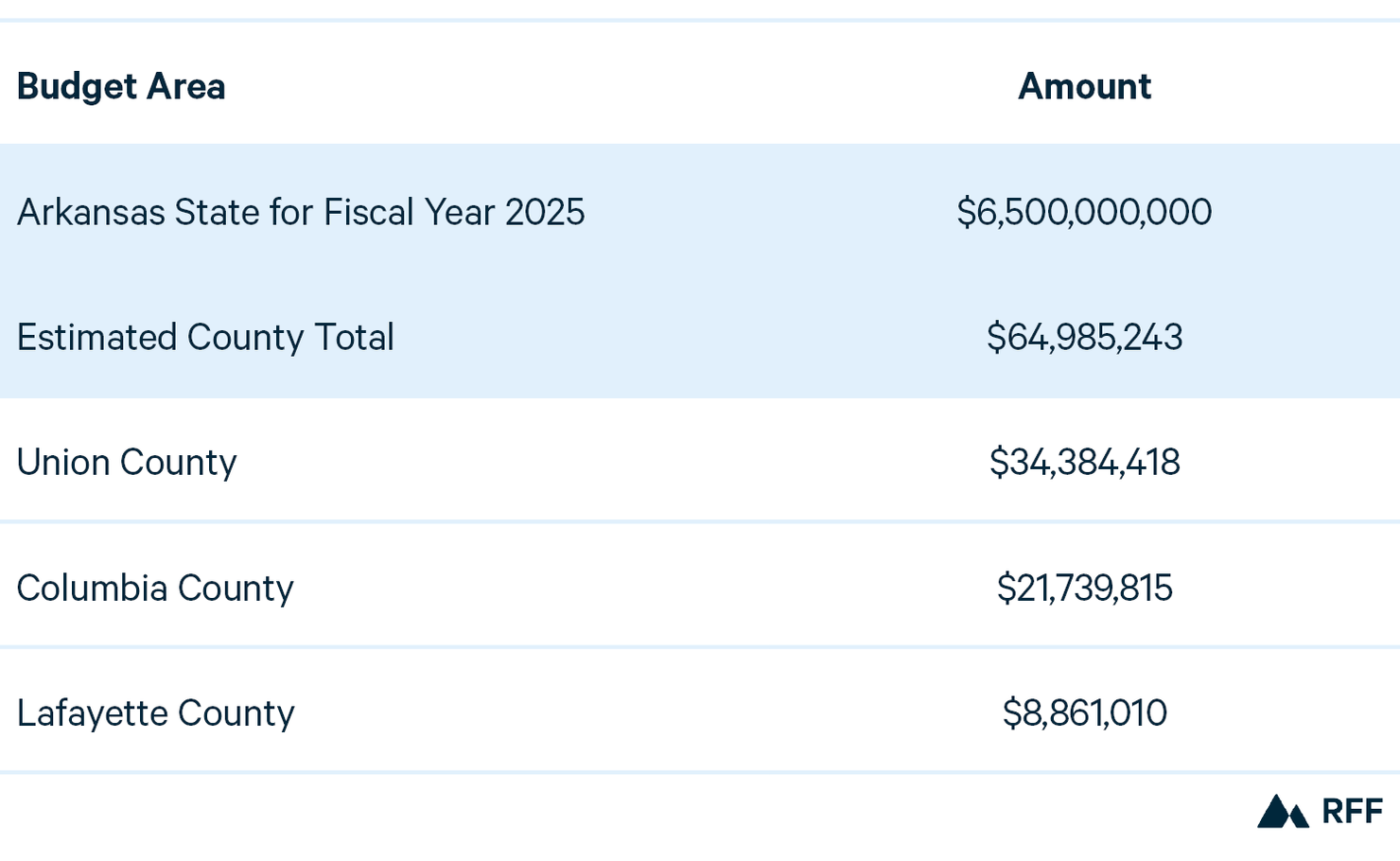

Table 4. Arkansas State and County Budgets