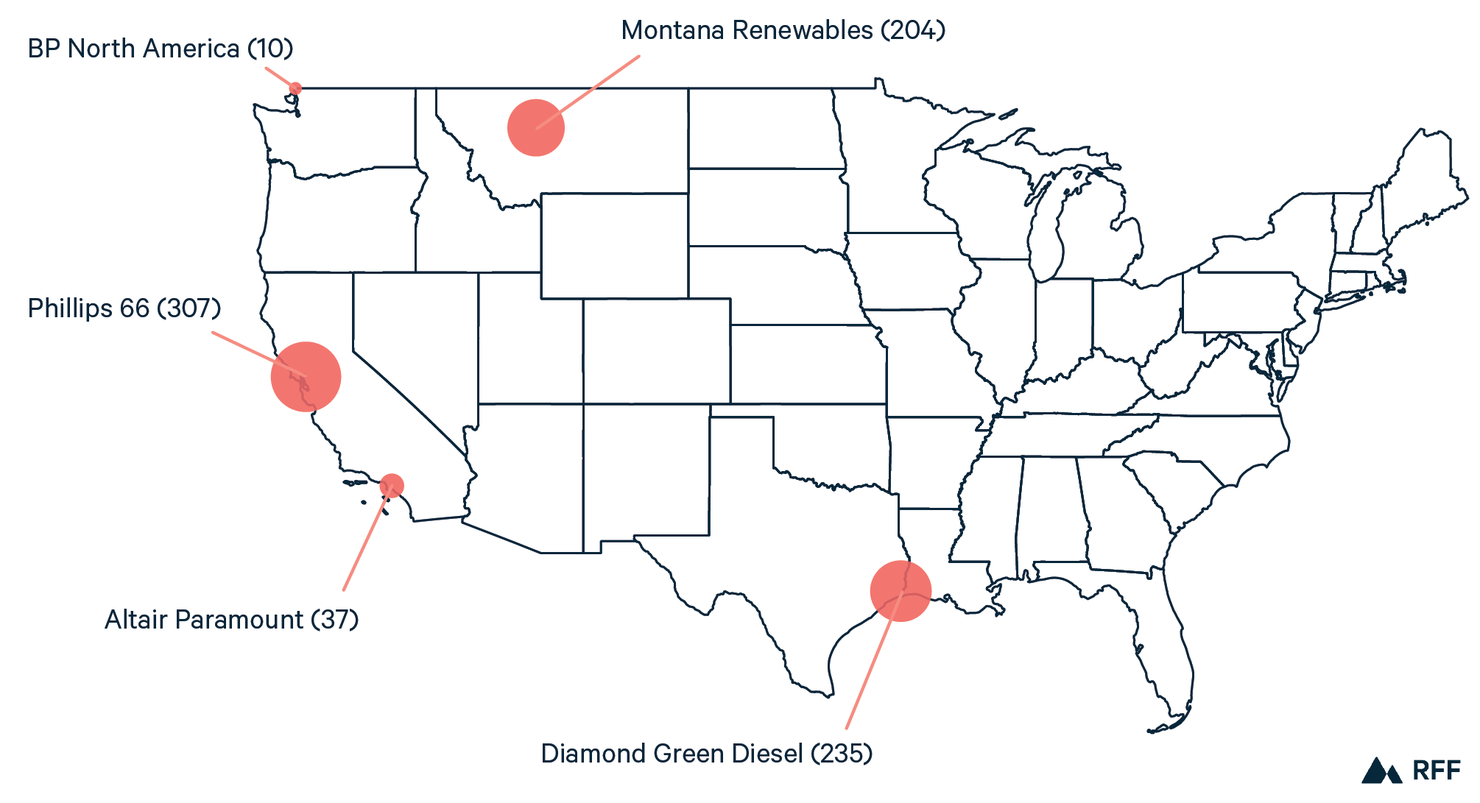

Figure 1. Locations of Facilities That Produce Sustainable Aviation Fuel Using the Hydroprocessed Esters and Fatty Acids Process

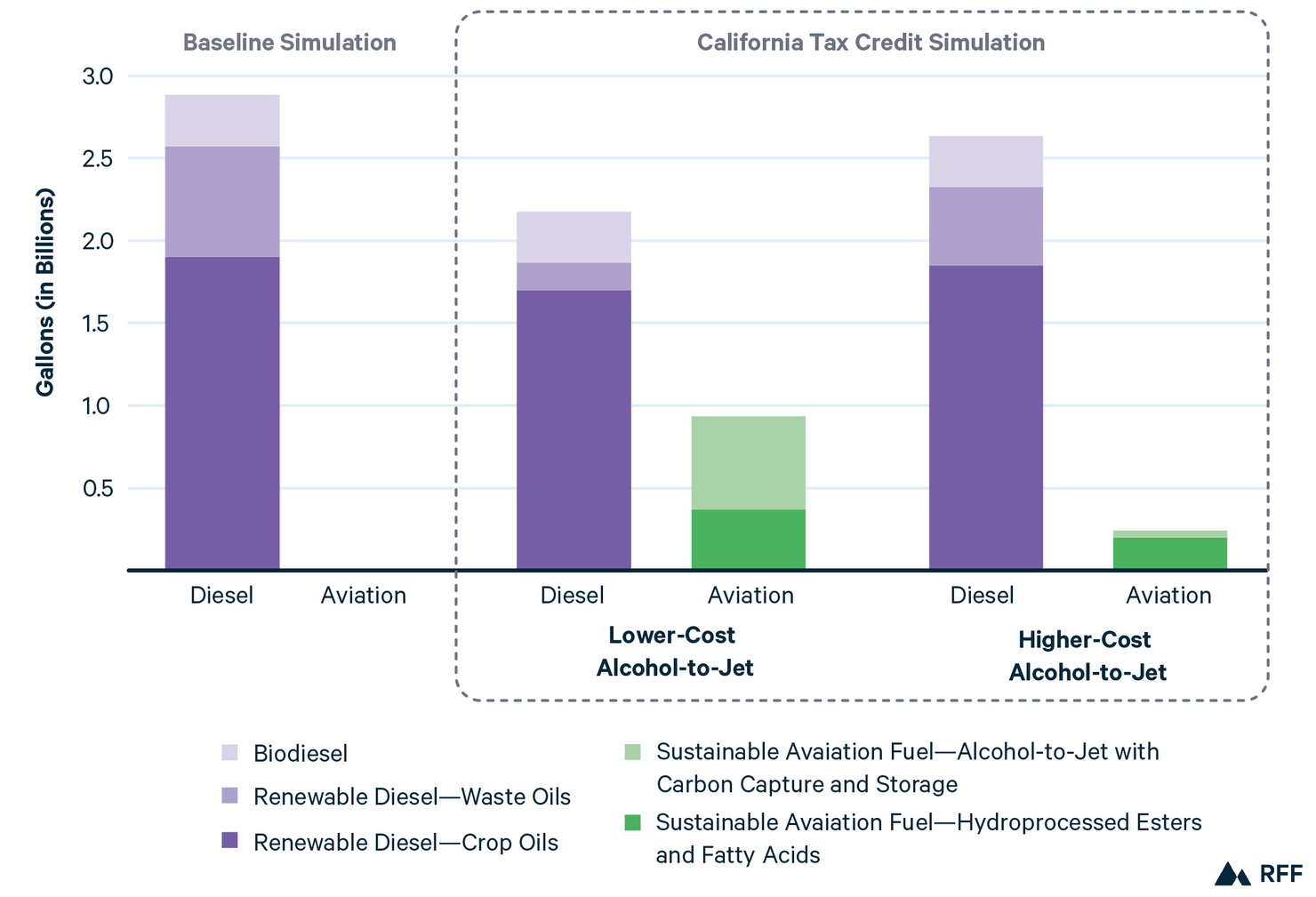

Figure 2. Quantity of Biofuels Used in Diesel and Aviation in California

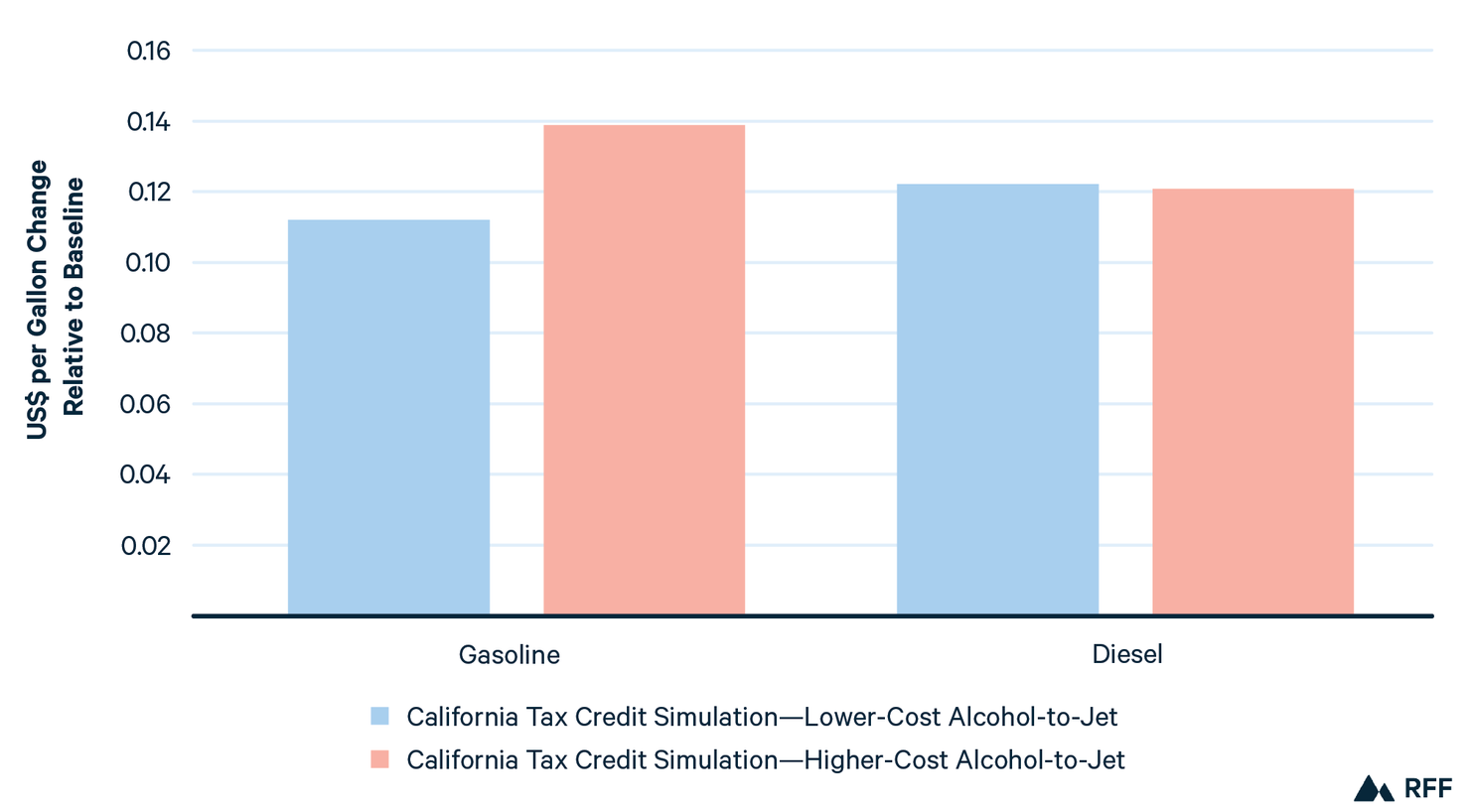

Figure 3. Change in Wholesale Fuel Prices

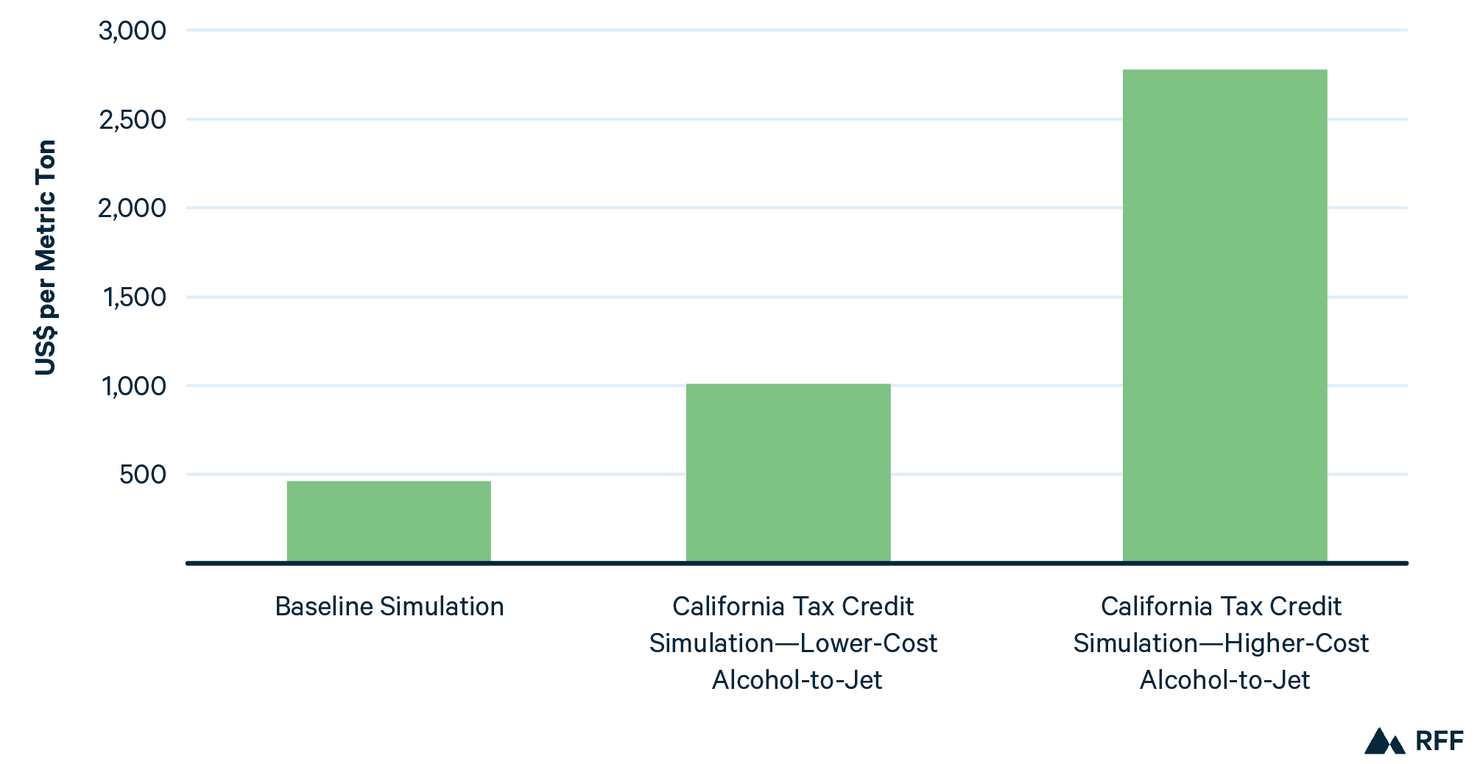

Figure 4. Average Cost of Reducing Carbon Dioxide Emissions