Global energy markets are in turmoil due to conflict in Iran. Although the United States is the top global oil and gas producer, it has limited options in relieving global supply strains.

The US and Israeli military strikes on Iran have sent global oil and gas markets spiraling. As oil prices hover near $100 per barrel, global attention is on the Strait of Hormuz, a narrow waterway through which flow enormous volumes of crude oil and liquefied natural gas (LNG). Shipments of oil and gas through the strait are at a standstill due to Iranian threats to tankers.

As we write, benchmark US crude prices hover near $95 per barrel (bbl), a significant rise from the prewar levels in the low- to mid-$60/bbl range. International prices for LNG have jumped more than 50 percent, although this spike has little direct effect on US consumers.

In this piece, we lay out several topics that we’ll be watching closely in the weeks and months ahead to understand the impacts of these developments for the US and global economy, and how policymakers might respond. Although we focus here on energy markets, we of course acknowledge the immense suffering that millions of people in the Middle East and elsewhere are now experiencing through a mix of direct violence, trauma, and exposure to toxic air pollution.

Energy Independence: Not an Actual Thing

For decades, US presidents have articulated a goal of energy “independence.” As we’ve written before, there is no such thing as energy independence, particularly when it comes to oil. Global oil markets are well integrated, so no matter how much oil the United States produces, a disruption in one part of the world (such as the Strait of Hormuz) will lead to a global spike in crude oil prices. Because the cost of crude oil is the most important determinant of the price of gasoline and diesel, and crude oil costs have soared, US drivers suddenly are facing higher prices at the pump. Although LNG trade has also been affected by disruptions in the Strait of Hormuz, natural gas markets are more fragmented, moderating the effects on prices for US consumers.

Some experts have argued correctly that wind and solar energy are not vulnerable to the same type of price volatility; as Resources for the Future (RFF) board member Catherine Wolfram put it, “you can’t weaponize the sun.” But clean energy technologies, including wind, solar, batteries, and electric vehicles, are not immune from supply chain disruptions stemming from geopolitical disputes. China’s restrictions on the export of critical minerals are a prime example of how energy independence is not an inevitable consequence of a transition to a low-emissions future. Going forward, policymakers should focus on energy security and diversification of supply chains, rather than the chimera of “independence.”

It’s Not All About Oil

Although oil disruptions are in the headlines, natural gas shipments and production in the Persian Gulf also are being disrupted. About 30 percent of natural gas consumption is traded internationally, two-thirds via pipeline and one-third by ship as LNG. It is the latter that has been disrupted by the war. Because of drone attacks, Qatar—a major LNG producer and exporter of around 10 billion cubic feet per day—shut down its production, cutting 20 percent of world LNG trade. Qatari producers shipped most of their LNG to Asia and the European Union, where LNG prices have roughly doubled in recent weeks.

Credit: Aerial-motion / Shutterstock

How can this huge price shock and the implied shortage be mitigated? One possible avenue is for the United States, as the world’s largest LNG exporter and major EU supplier, to step up shipments. Construction is underway to expand US export capacity, but most of these facilities will come online in the coming years, not weeks or months. US producers and exporters might want to expand exports from current facilities, particularly given the huge price premium, but LNG export facilities typically operate near full capacity, so there’s little room to grow there. Other major exporters such as Australia might be able to help a bit, but LNG trade is often determined well in advance through long-term contracts, which are needed to secure financing for multibillion-dollar LNG plants. This dynamic limits the availability of cargoes on spot markets. However, over the past decade, LNG contracts have provided more flexibility for buyers and sellers, suggesting more latitude to shift shipments as needed than was possible previously.

Another possible pathway to reduce EU natural gas prices would be through the European Union’s own natural gas inventories, which typically are drawn down in the winter from heating demands and then replenished during other periods. But EU gas storage levels are largely depleted, and sit well below their historical averages, making large withdrawals unlikely. With links to Russia largely severed since 2022, depleted natural gas inventories put the Europeans in a particularly challenging position.

Is a Spike in Oil Prices Good or Bad for the US Economy?

In the first decade of the 2000s, spikes in global oil prices had clear negative impacts for the US economy. The country produced five or six million barrels per day (mb/d) while consuming closer to 20 mb/d. The United States was the world’s largest importer of crude oil, so high prices meant more dollars flowing out of the United States and toward exporters such as Canada, Mexico, and Saudi Arabia.

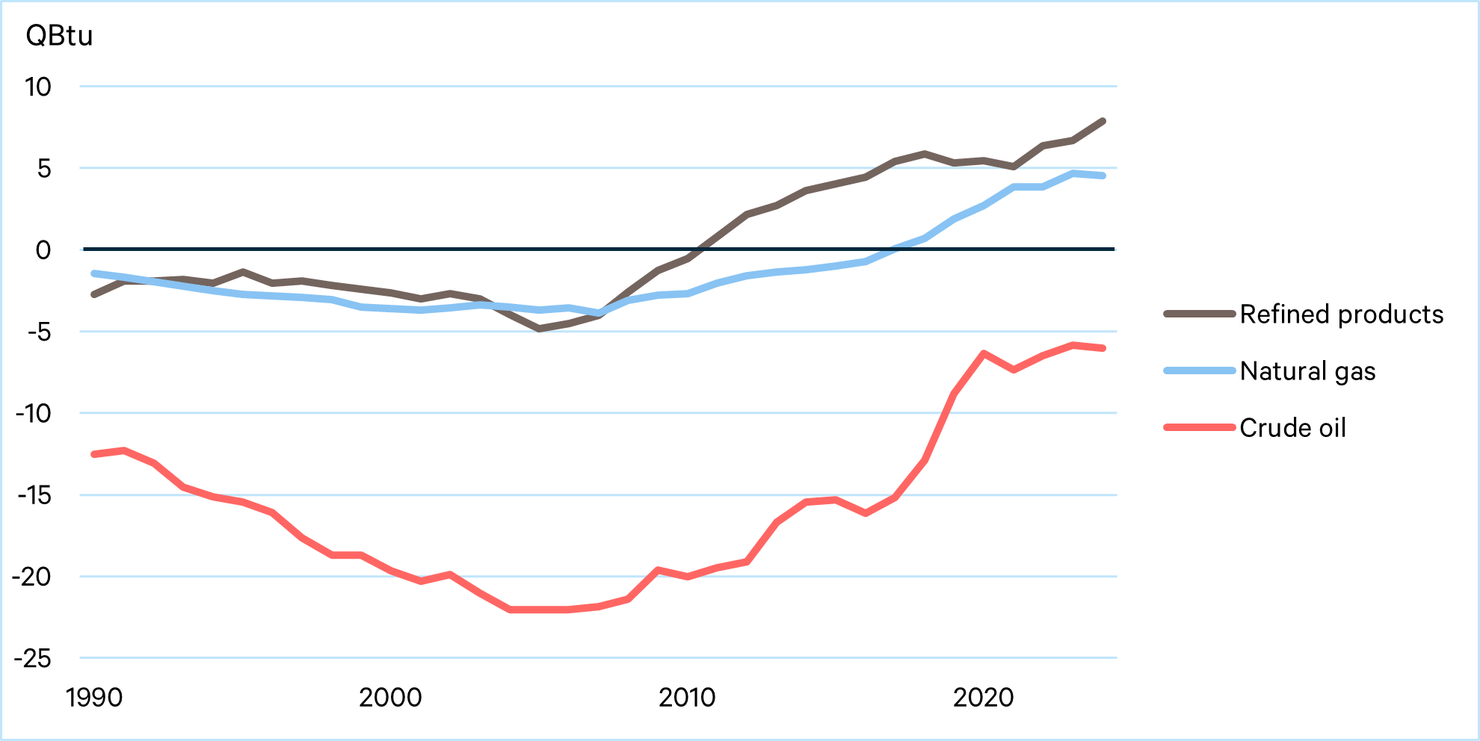

Today, the United States is the world’s largest producer of oil and gas and a major exporter of both fuels. In 2024, the United States exported 28 quadrillion British thermal units (QBtu) of crude oil, refined petroleum products, and natural gas, and imported 21 QBtu. (For reference, Saudi Arabia’s total energy production in 2024 was about 27 QBtu.) As shown in Figure 1, this level of exports is a stark change from decades past, when the United States imported much more than it shipped abroad. In the aggregate, these data suggest that higher oil and natural gas prices could potentially boost, rather than dent, domestic GDP on net.

But there is nuance and uncertainty here. Higher oil prices—even when the United States is a net exporter—raise costs for individuals and businesses across the country and harm the day-to-day functioning of the economy. Higher gasoline prices also increase diesel prices, which in turn raise shipping costs, pushing product prices higher and contributing to inflationary pressure. Indeed, the odds of a US recession occurring this year have jumped substantially in recent weeks, according to certain prediction markets.

Figure 1. US Net Exports of Crude Oil, Refined Products, and Natural Gas

Data source: US Energy Information Administration, Tables 1.4a and 1.4b

But the domestic impacts of higher prices won’t be felt uniformly. Major oil- and gas-producing states such as Texas, New Mexico, North Dakota, Oklahoma, Alaska, and Wyoming will be buoyed by surging prices, while major consumers like New York, Florida, and Illinois will bear the brunt. Effects will vary within states, too. For example, as a whole, Californians will suffer from higher oil prices, while many residents of Kern County, a major oil producer in the state’s Central Valley, will welcome the windfall. Tribal, state, and local governments where oil and gas production occurs at scale also will see a bump in revenue from severance taxes, leases on publicly owned lands, property taxes, and other revenue sources linked directly to oil and gas production.

Regardless of the distributional impacts within the United States, high gasoline prices are political poison.

Regardless of the distributional impacts within the United States, high gasoline prices are political poison. Drivers from coast to coast are constantly reminded of gasoline prices at supersized digital displays dotting intersections and interstates. And although presidents usually have little control over the price of gasoline, voters tend to blame incumbent presidents when fuel prices soar.

US Supply to the Rescue? Unlikely.

With US production at all-time highs, can the country act as the “swing producer” to fill the gap left by the disruption in the Strait of Hormuz? This scenario is unlikely for various reasons. First, despite being the largest producer, total US crude production amounts to nearly 14 million barrels per day. An impressive level to be sure, but even if it doubled overnight, it would not cover the 20 million barrels per day of supply no longer flowing through the Strait of Hormuz.

But second and more fundamentally, US producers cannot simply “turn the taps” to increase production on a dime like some other producers, particularly Saudi Arabia. This is because existing oil wells in the United States tend to operate at maximum capacity, so increased production requires investments in new wells, which can take months or years to produce oil, given the time needed to drill, frack, and complete wells. RFF research has shown that while US oil supply is much more price responsive due to the shale boom, the inertia in the system implies that meaningful supply responses to price fluctuations can take six months to two years—far too slow to play the role of “swing producer.”

Third, US drillers are likely to make new investments only if they expect today’s high prices to last. Oil and gas producers can either roll the dice on the spot market or lock in hedges by selling oil futures for delivery when they expect their drilling to eventually yield oil—say, in six months. But the run-up in crude oil prices has been limited to spot prices and the first few months of the futures strip, resulting in prices for near-term delivery exceeding prices for delivery further in the future. This unusual timeline for prices is called “backwardation.”

While prices for crude delivered in the next few weeks (also called front-month prices) for West Texas Intermediate fluctuated wildly between $80 and $120 per barrel on March 9, the price for delivery in September has remained fairly stable at around $75–$80 per barrel, perhaps in anticipation that the supply disruption will be relatively short lived. While this $75–$80 price level is somewhat elevated from prewar levels and could produce some incremental oil production, a surge of US drilling or supply is unlikely. Indeed, in the two weeks between February 27 (the day before strikes on Iran began) and March 13, the US rig count from Baker Hughes rose by merely three rigs—from 550 to 553, a 0.5 percent increase.

Can Strategic Oil Reserves Save the Day?

If US supply isn’t going to fill the gap anytime soon, what about strategic oil reserves? The United States and other nations hold these reserves, which are designed to provide a buffer during times of emergency disruption. RFF research has argued that the above-mentioned backwardation in the crude oil futures strip makes a good argument that market participants expect oil supply disruptions to be transitory, which strengthens the case for the use of strategic reserves as an emergency release.

In recent days, the International Energy Agency and United States have announced releases on the order of 400 million barrels. Although this is the largest such release in history, it is equivalent to about four days’ worth of global supply, or about 20 days’ worth of the amount currently disrupted in the Strait of Hormuz (20 million barrels per day). Given these volumes, it is perhaps not surprising that oil markets did not react strongly to the news.

The Takeaway

Although the United States is a leading oil and gas exporter, higher global oil and gas prices remain a political liability, rather than an asset, for any federal administration. This negative outlook is due primarily to the globally integrated nature of oil markets and the heavy dependence of the US transportation sector on gasoline, diesel, and jet fuels.

Looking forward, a shift away from petroleum products can help insulate the United States from short-term volatility in fuel prices. But such a shift to zero- and lower-emissions energy technologies will not make the energy system immune to geopolitical forces. Instead, such a transition will come with the need to diversify supply chains, work closely with allied countries, and develop new technologies that can enhance energy security while ensuring affordable, reliable energy for US consumers.